Buy Now

3D Printing Gases Market Size, Share, Growth & Industry Analysis, By Product (Argon, Nitrogen, Gas Mixtures), By Technology (Stereolithography, Laser Sintering, Poly-jet technology, Others), By Application (Design and Manufacturing, Healthcare, Consumer Products, Others), and Regional Analysis, 2024-2031

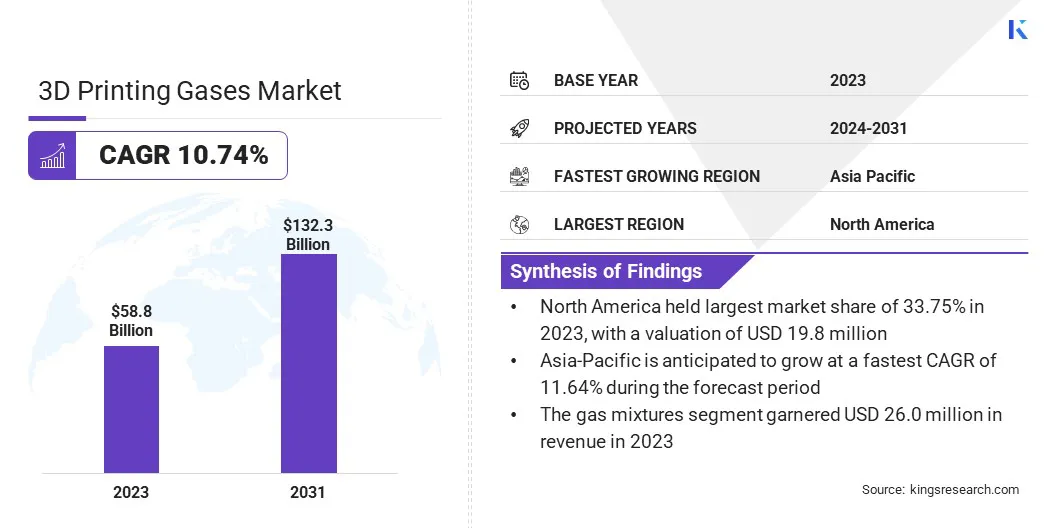

Pages: 180 | Base Year: 2023 | Release: March 2025 | Author: Versha V.

The 3D printing gases market encompasses the supply and use of specialized gases essential for additive manufacturing processes. These gases, including inert gases such as argon, nitrogen, and helium, along with reactive gases like oxygen, are crucial for controlling the atmosphere during the 3D printing process to ensure optimal material properties and precision while preventing oxidation.

The global 3D printing gases market size was valued at USD 58.8 billion in 2023 and is projected to grow from USD 64.8 billion in 2024 to USD 132.3 billion by 2031, exhibiting a CAGR of 10.74% during the forecast period.

The market is experiencing significant growth driven by advancements in additive manufacturing technologies, increasing adoption across industries such as aerospace, automotive, healthcare, and electronics, and rising demand for high-performance materials.

Major companies operating in the global 3D printing gases industry are Air Liquide, Linde PLC, Air Products and Chemicals, Inc, Messer SE & Co. KGaA, Gaztron, ExOne, Velo3D, TAIYO NIPPON SANSO CORPORATION, Coregas, SOL Group, Airgas, Inc., BASF, EOS GmbH, Materialise, and Nikon SLM Solutions AG.

The growing shift toward customized and complex designs, coupled with the development of new materials and 3D printing techniques, is expected to further propel market growth. Factors such as rising industrial automation, the shift toward digital manufacturing, and the expansion of 3D printing applications in emerging economies are also contributing to market expansion.

Market Driver

"Advancements in Additive Manufacturing Technologies"

Advancements in additive manufacturing technologies is propelling the growth of the 3D printing gases market. Techniques such as metal additive manufacturing, selective laser melting, and direct energy deposition require precise atmospheric control to ensure material integrity and quality.

Gases such as argon, nitrogen, and hydrogen help prevent oxidation and optimize material fusion, particularly in high-performance sectors such as aerospace and healthcare.

The development of advanced printing technologies allows for the use of a broader range of materials, including advanced alloys and composites, which often require specific gas mixtures for processing.

Market Challenge

"High Cost of Specialized Gases"

A significant challenge hampering the growth of the 3D printing gases market is the high cost of specialized gases. Gases such as argon, nitrogen, and helium are essential for maintaining controlled environments during additive manufacturing processes, particularly in high-precision applications such as 3D printing metal. However, these gases are often expensive, especially when required in large quantities or for extended periods.

The need for high-purity gases and specific gas mixtures further increases their cost. This financial burden can make 3D printing less accessible to small and medium-sized businesses or industries with tight budgets, limiting the widespread adoption of advanced 3D printing technologies.

This challenge can be addressed by optimizing gas usage through efficient gas flow systems and minimizing waste to lower costs. Advanced gas management systems that provide precise control over gas mixtures can help reduce consumption and overall expenditure.

Additionally, exploring cost-effective gases or gas blends that meet application requirements without compromising quality. Manufacturers can also benefit from negotiating long-term contracts or bulk purchases with gas suppliers to secure better pricing.

Market Trend

"Advancements in Gas Recycling Technologies"

Advancements in gas recycling technologies are emerging as a significant trend in the 3D printing gases industry as companies seek to reduce costs and improve environmental sustainability. These technologies capture, purify, and reuse gases typically wasted during the printing process, leading to cost savings and a reduced environmental footprint.

Systems that recover inert gases, such as nitrogen and argon, commonly used in metal 3D printing, can be integrated into manufacturing setups to continuously cycle and reuse these gases. Advancements in filtration and purification technologies ensure that recycled gases maintain the high purity required for specific 3D printing applications, preserving print quality.

|

Segmentation |

Details |

|

By Product |

Argon, Nitrogen, Gas Mixtures |

|

By Technology |

Stereolithography, Laser Sintering, Poly-jet technology, Others |

|

By Application |

Design and Manufacturing, Healthcare, Consumer Products, Others |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe |

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific |

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

|

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America 3D printing gases market share stood at around 33.75% in 2023, with a valuation of USD 19.8 million. This dominance is attributed to the strong presence of key players, significant investments in R&D, and the rapid adoption of 3D printing technologies across various sectors, including aerospace, automotive, and healthcare.

The region’s well-established manufacturing infrastructure and increasing focus on innovation in 3D printing materials and processes are further fueling regional market growth.

Asia-Pacific 3D printing gases industry is poised grow at a robust CAGR of 11.64% over the forecast period, supported by rapid industrialization, increasing adoption of additive manufacturing technologies, and the rising demand for 3D-printed products in sectors such as automotive, electronics, and healthcare.

The region's expanding manufacturing base, particularly in countries such as China, Japan, and South Korea, along with favorable government initiatives promoting innovation and digital manufacturing, are key factors contributing to this growth.

The competitive landscape of the 3D printing gases market is defined by a range of participants, from established industrial gas suppliers to specialized companies providing bespoke solutions tailored to the needs of the additive manufacturing sector.

Market players are placing a strong emphasis on expanding their product portfolios, improving the performance characteristics of 3D printing gases, and ensuring the availability of high-purity gases to enhance print quality, production speed, and material properties.

Recent Developments (New Product Launch/Agreements)

Frequently Asked Questions