Aerospace and Defense

Data Relay Satellite Market

Data Relay Satellite Market Size, Share, Growth & Industry Analysis, By Payload Type (Radio-frequency (RF), Optical, Electronic), By Application (Earth Observation, Space Exploration, Meteorology, Emergency Management, Others), By End-Use (Commercial, Government, Military), and Regional Analysis, 2024-2031

Pages : 180

Base Year : 2023

Release : April 2025

Report ID: KR1617

Market Definition

The market involves the development, production, and operation of satellites that transmit data between spacecraft, ground stations, and other satellites. These satellites facilitate continuous and real-time communication, particularly for Earth observation, scientific missions, military operations, and commercial uses.

Data Relay Satellite Market Overview

The global data relay satellite market size was valued at USD 8,230.0 million in 2023 and is projected to grow from USD 8,882.8 million in 2024 to USD 16,364.5 million by 2031, exhibiting a CAGR of 9.12% during the forecast period.

Market growth is driven by increasing demand for efficient communication systems in space missions, rising investments in satellite-based services, and advancements in satellite technology. This expansion is further fueled by the rising demand for real-time data transmission in remote sensing, scientific research, Earth observation, and defense applications.

Major companies operating in the data relay satellite industry are SES S.A, Boeing, EUTELSAT COMMUNICATIONS SA, Northrop Grumman, RESHETNEV, Thales Alenia Space, EUROPEAN SPACE AGENCY., Maxar Technologies, SpaceLink, EchoStar Mobile Ltd, ispace, Telesat, Thales, Sidus Space, and KONGSBERG SATELLITE SERVICES.

The increasing involvement of private sector and international collaborations in space exploration is expected to boost the adoption of data relay satellites, enhancing global connectivity and operational efficiency.

- In June 2024, TTP plc, in partnership with Surrey Satellite Technology Ltd. (SSTL), launched an intersatellite data relay terminal for Low Earth Orbit (LEO) SmallSats. This terminal enables continuous data communication with Earth through a geosynchronous satellite relay, enabling on-demand, real-time data transfer and enhanced satellite control.

Key Highlights

- The data relay satellite industry size was recorded at USD 8,230.0 million in 2023.

- The market is projected to grow at a CAGR of 9.12% from 2024 to 2031.

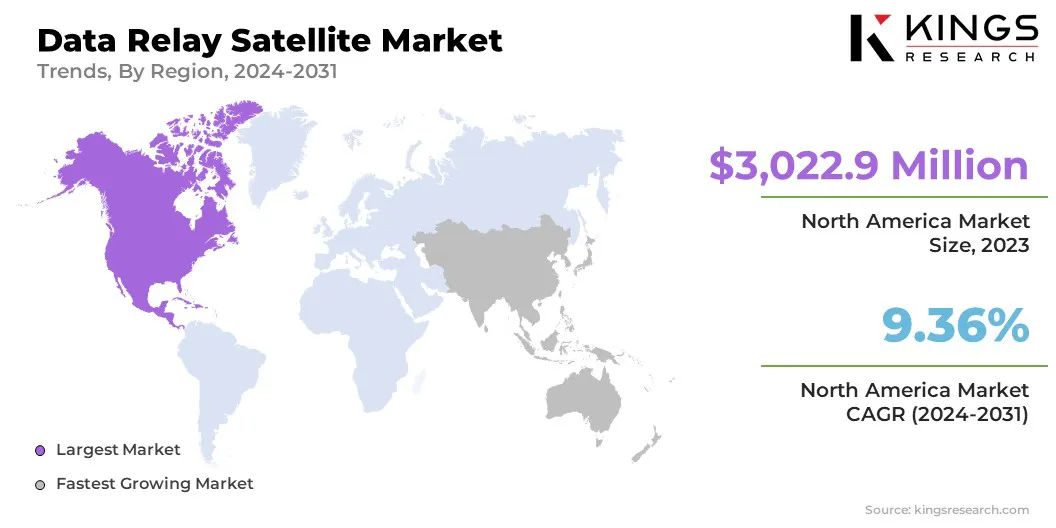

- North America held a share of 36.73% in 2023, valued at USD 3,022.9 million.

- The radio-frequency (RF) segment garnered USD 3,729.8 million in revenue in 2023.

- The earth observation segment is expected to reach USD 6,504.6 million by 2031.

- The commercial segment is anticipated to witness the fastest CAGR of 9.60% over the forecast period.

- Asia Pacific is anticipated to grow at a CAGR of 9.88% through the projection period.

Market Driver

Advancements in Satellite Technology

Advancements in satellite technology are fueling the growth of the data relay satellite market. Developments in miniaturization, payload capacity, and energy efficiency have enhanced satellite capabilities while reducing costs.

Innovations in optical communication systems and advanced radio-frequency technologies are improving data transfer speed, reliability, and latency. Additionally, the integration of artificial intelligence (AI) and machine learning in satellite operations is enabling better data processing and management.

- In January 2025, Japan Aerospace Exploration Agency NEC Corporation achieved the world's fastest optical communication using the Laser Utilizing Communication System (LUCAS) between the Advanced Land Observing Satellite-4 (ALOS-4) and an Optical Data Relay Satellite in geostationary orbit.

Market Challenge

Technological Complexity and Interoperability

Technological complexity and interoperability challenge significantly impact the data relay satellite market.Aas satellites integrate advanced technologies such as optical communication, artificial intelligence, and advanced payloads, design, integration, and operational requirements become increasingly intricate.

Managing these systems requires specialized expertise, leading to higher costs, longer development times, and increased failure risks. Ensuring seamless interoperability between satellite platforms, ground stations, and communication networks is essential. Aligning different satellite models and technologies remains a challenge, leading to deployment delays and reduced service flexibility.

To address these issues, industry players are investing in standardized protocols and open architectures for seamless integration across satellite platforms, ground stations, and networks.

Collaboration between stakeholders to establish common standards, along with continuous R&D to simplify satellite design and integration, can reduce technical barriers. Adopting modular, scalable architectures will enhance adaptability to emerging technologies, improving operational efficiency and service delivery.

Market Trend

Expansion of Low Earth Orbit (LEO) Satellites

A key trend influencing the market is the rising deployment of low earth orbit (LEO) satellites due to their advantages in faster, more cost-effective, and frequent data transmission. Positioned closer to Earth than geostationary satellites, LEO satellites reduces latency and improves communication speeds, essential for real-time data relay.

This expansion is fueled by the rising need for global connectivity, particularly in remote regions, where LEO satellites offer more accessible solutions for internet and communication services. The deployment of large LEO satellite constellations has created new opportunities for continuous global data relay services in sectors such as Earth observation, scientific research, and telecommunications.

- In June 2024, SES S.A. Space & Defense successfully demonstrated the first multi-orbit, multi-band commercial LEO relay, showcasing its ability to provide flexible, low-latency satellite communications across multiple orbital platforms. This demonstration enahnces telecommunications, defense, and global connectivity.

Data Relay Satellite Market Report Snapshot

|

Segmentation |

Details |

|

By Payload Type |

Radio-frequency (RF), Optical, Electronic |

|

By Application |

Earth Observation, Space Exploration, Meteorology, Emergency Management, Others (Search and Rescue, Environmental Monitoring) |

|

By End-Use |

Commercial, Government, Military |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe |

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific |

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

|

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation

- By Payload Type (Radio-frequency (RF), Optical, and Electronic): The radio-frequency (RF) segment earned USD 3,729.8 million in 2023 due to its widespread use in communication and data transmission applications.

- By Application (Earth Observation, Space Exploration, Meteorology, Emergency Management, and Others (Search and Rescue and Environmental Monitoring)): The earth observation segment held a share of 37.53% in 2023, mainly fueled by the increasing demand for real-time environmental monitoring and data collection for climate studies, agriculture, and disaster management.

- By End-Use (Commercial, Government, and Military): The commercial segment is projected to reach USD 5,472.5 million by 2031, propelled by the growing demand for satellite communication, data services, and connectivity solutions across various industries.

Data Relay Satellite Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America data relay satellite market share stood at around 36.73% in 2023, valued at USD 3,022.9 million. This dominance is attributed to the presence of key players in satellite technology, significant investments in space exploration, and a strong demand for advanced communication systems from both government and commercial sectors.

North America's robust space infrastructure, with numerous ground stations and satellite manufacturers, further supports this growth. The growing use of satellite-based services for telecommunications, Earth observation, and defense is fostering regional market expansion.

- In April 2024, ispace technologies U.S., inc. announced a data relay service utilizing two satellites, set for deployment in Mission 3 in 2026. These satellites will facilitate communication between Earth and lunar missions, including the APEX 1.0 lunar lander.

Asia-Pacific market is estimated to grow at a CAGR of 9.88% over the forecast period. This growth is fueled by higher investments in space infrastructure, growing demand for satellite communication services, and a surge in space exploration activities.

The region’s growing dependence on satellite-based services for telecommunications, remote sensing, and disaster management, along with new space initiatives in China, India, and Japan, further stimulates regional market expansion.

Regulatory Frameworks

- In the U.S., The Federal Communications Commission (FCC) regulates the Tracking and Data Relay Satellite System (TDRSS) to ensure proper satellite communication for space operations. The regulation addresses licensing, frequency coordination, and operational standards, aiming to maintain secure and efficient data relay services for government and commercial missions.

- The Federal Aviation Administration (FAA) regulates satellite operations under Title 14, Chapter V, Part 1215, outliing licensing procedures for commercial space launches and satellite communications.

- The Federal Communications Commission (FCC) regulates Non-Geostationary Orbit (NGSO) satellite constellations to manage spectrum use, prevent interference, and support sustainable satellite operations.

Competitive Landscape

The data relay satellite industry is characterized by a competitive landscape with various players focused on technological advancements and innovation. Companies are increasingly adopting advanced systems such as optical communication and AI to address challenges like satellite interference and space debris.

Market players further focus on forming strategic alliances to expand their reach and enhance their service portfolios, responding to the growing demand for global connectivity and data relay services.

- In March 2025, Sidus Space launched LizzieSat-3, a satellite equipped with AI-driven capabilities for space-to-space data relay. This next-generation satellite aims to offer real-time intelligence processing in Low Earth Orbit (LEO) with reduced latency and automated decision-making, marking a significant advancement in AI-powered space solutions.

List of Key Companies in Data Relay Satellite Market:

- SES S.A

- Boeing

- EUTELSAT COMMUNICATIONS SA

- Northrop Grumman

- RESHETNEV

- Thales Alenia Space

- EUROPEAN SPACE AGENCY.

- Maxar Technologies

- SpaceLink

- EchoStar Mobile Ltd

- ispace

- Telesat

- Thales

- Sidus Space

- KONGSBERG SATELLITE SERVICES

Recent Developments (M&A/Partnerships/Agreements/New Product Launch)

- In November 2024, Kepler Communications Inc. announced a strategic shift in its strategy for its optical data relay network. The company filed with the FCC to consolidate its constellation size and integrate advanced optical technology, transitioning from RF technology.

- In March 2024, Viasat, Inc. and Rocket Lab USA, Inc. partenered to showcase on-demand, low-latency data relay services for Low Earth Orbit (LEO) satellites. This collaboration aims to improve communication capabilities by reducing data latency and enabling real-time data relay via Viasat’s Ka- and L-band networks.

CHOOSE LICENCE TYPE

CUSTOMIZATION OFFERED

Additional Company Profiles

Additional Company Profiles- Additional Countries

- Cross Segment Analysis

- Regional Market Dynamics

- Country-Level Trend Analysis

- Competitive Landscape Customization

- Extended Forecast Years

- Historical Data Up to 5 Years

.webp)