Advanced Materials and Chemicals

Electric Vehicle Adhesive Market

Electric Vehicle Adhesive Market Size, Share, Growth & Industry Analysis, By Adhesive Type (Structural Adhesives, Hot Melt Adhesives, Pressure-Sensitive Adhesives, Polyurethane Adhesives, Acrylic Adhesives, Epoxy Adhesives), By Substrate (Metal, Plastics, Composite Materials), By Vehicle Type, By Application, and Regional Analysis, 2024-2031

Pages : 210

Base Year : 2023

Release : March 2025

Report ID: KR1551

Market Definition

The Electric Vehicle (EV) adhesive market encompasses the development and supply of advanced bonding solutions specifically formulated for EV manufacturing. These adhesives are engineered using structural epoxies, Polyurethane (PU), acrylics, and silicone-based formulations to meet the unique thermal, mechanical, and electrical insulation demands of EV components.

They play a crucial role in battery pack assembly, electric motor bonding, power electronics encapsulation, and lightweight vehicle structures, replacing traditional mechanical fasteners to enhance durability and crash resistance.

Adhesives also contribute to thermal management, sealing, and vibration damping in EVs, ensuring optimal performance and longevity of high-voltage systems while supporting the industry's push toward weight reduction and improved energy efficiency.

Electric Vehicle Adhesive Market Overview

The global electric vehicle adhesive market size was valued at USD 1,568.3 million in 2023 and is projected to grow from USD 1,869.8 million in 2024 to USD 7,347.0 million by 2031, exhibiting a CAGR of 21.59% during the forecast period. The market is driven by the increasing adoption of lightweight materials to enhance vehicle efficiency and extend battery range.

Advanced adhesive solutions are replacing traditional fasteners, enabling structural integrity while reducing overall weight. Additionally, the rising demand for high-performance thermal management in EV batteries is fueling the development of adhesives with superior thermal conductivity, ensuring safety, durability, and enhanced battery performance.

Major companies operating in the global electric vehicle adhesive industry are Henkel Corporation, H.B. Fuller Company, Sika AG, 3M, PPG Industries, Inc., Evonik, Arkema, Dow, Huntsman International LLC, BASF, Bostik, Wacker Chemie AG, Ashland, Saint-Gobain, and Parker Hannifin Corp.

The shift toward lightweight vehicle structures is accelerating the growth of the market. Automakers are increasingly utilizing structural adhesives to replace conventional mechanical fasteners, reducing overall vehicle weight while enhancing energy efficiency. These adhesives distribute stress more evenly, improving crash resistance and durability.

The adoption of lightweight composite materials in EVs necessitates advanced bonding solutions that ensure structural integrity without adding excess weight. Additionally, reduced weight contributes to extended battery range and overall vehicle performance, making high-performance adhesives essential in modern EV designs.

Key Highlights:

- The global electric vehicle adhesive market size was valued at USD 1,568.3 million in 2023.

- The market is projected to grow at a CAGR of 21.59% from 2024 to 2031.

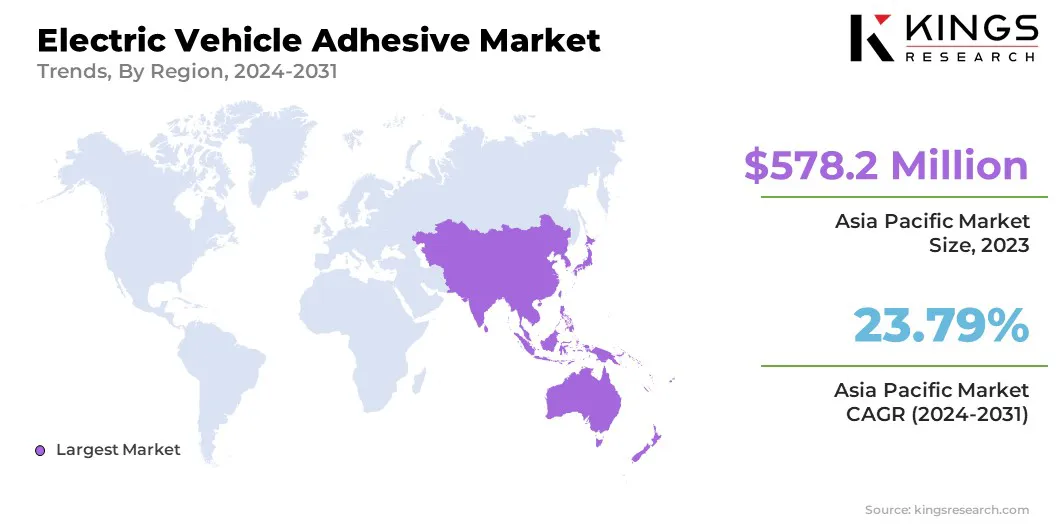

- Asia Pacific held a market share of 36.87% in 2023, with a valuation of USD 578.2 million.

- The structural adhesives segment garnered USD 377.8 million in revenue in 2023.

- The battery assembly segment is expected to reach USD 2,133.5 million by 2031.

- The metal segment secured the largest revenue share of 40.12% in 2023.

- The hybrid electric vehicles (HEVs) is poised for a robust CAGR of 24.07% through the forecast period.

- The market in North America is anticipated to grow at a CAGR of 22.26% during the forecast period.

Market Driver

"Growth in EV Production"

The rapid expansion of EV manufacturing globally is significantly boosting the electric vehicle adhesive market. Leading automakers are ramping up EV production through strategic investments, new manufacturing facilities, and partnerships, creating substantial demand for advanced adhesives.

- The 2024 International Energy Agency (IEA) report indicates that nearly 14 million new electric cars were registered globally in 2023, raising the total number of EVs on the road to 40 million. Electric car sales in 2023 registered an increase of 3.5 million units compared to 2022, reflecting a 35% year-on-year growth. This figure represents more than a sixfold rise from 2018 levels within just five years. Battery electric vehicles (BEVs) made up 70% of the global electric car stock in 2023, highlighting their dominance in the expanding EV market.

Government incentives, carbon neutrality targets, and emission regulations are further accelerating EV adoption, driving the need for durable, high-performance adhesives that enhance vehicle longevity and efficiency. Adhesive manufacturers are scaling operations to meet the growing industry demand as production volumes increase.

- In February 2023, Dow introduced the next-generation Voratron MA 8200S thermal elastic high-bonding adhesives at the 5th China International Import Expo (CIIE 2022). These advanced adhesives are engineered to enhance the safety, durability, sustainability, and integrated assembly of EV battery packs while improving overall performance. It is specifically designed for bonding cells with insulating bottom shells, upper cover plates, and side plate stiffeners, including applications for electrified E2 platform cells, such as bottom high-bonding, upper cover high-bonding, and side panel high-bonding adhesives.

Market Challenge

"Adhesion Performance Under Extreme Conditions"

A significant challenge in the electric vehicle adhesive market is ensuring adhesion reliability under extreme environmental conditions, including high temperatures, humidity, and mechanical stress. Variations in thermal expansion between bonded materials can lead to adhesive degradation, impacting structural integrity and battery safety.

Several manufacturers are developing next-generation adhesive formulations with enhanced thermal stability, flexibility, and mechanical strength. Innovations such as high-temperature-resistant adhesives and dual-curing systems are improving long-term performance.

Additionally, companies are investing in rigorous testing protocols and advanced simulation techniques to optimize adhesion properties and ensure durability across varying operating conditions.

Market Trend

"Advancements in Battery Technology"

Continuous advancements in EV battery technology are fueling the electric vehicle adhesive market. High-performance adhesives play a critical role in battery pack assembly, cell-to-cell bonding, and thermal interface materials, ensuring mechanical stability and heat dissipation.

The increasing focus on battery safety and longevity has led to the adoption of flame-retardant and thermally conductive adhesives that prevent overheating and enhance energy efficiency.

The demand for specialized adhesives with superior electrical insulation and chemical resistance rises as battery designs evolve to incorporate solid-state and high-energy-density cells, reinforcing their importance in next-generation EV manufacturing.

- In November 2024, Parker Hannifin launched CoolTherm TC-2002, a two-component adhesive system designed to deliver exceptional thermal conductivity, optimizing heat dissipation in EV battery components. This advanced adhesive minimizes the risk of overheating by improving heat transfer, enhancing battery lifespan and operational safety. Engineered to address key challenges in industrial EV batteries, CoolTherm focuses on critical aspects such as thermal management, performance reliability, and long-term durability, making it a vital solution for improving battery efficiency and safety in EVs.

Electric Vehicle Adhesive Market Report Snapshot

|

Segmentation |

Details |

|

By Adhesive Type |

Structural Adhesives, Hot Melt Adhesives, Pressure-sensitive Adhesives, Polyurethane Adhesives, Acrylic Adhesives, Epoxy Adhesives, Silicone Adhesives |

|

By Substrate |

Metal, Plastics, Composite Materials |

|

By Vehicle Type |

Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs) |

|

By Application |

Battery Assembly, Exterior & Body Structure, Interior Components, Powertrain & Electronics |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe |

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific |

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

|

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation:

- By Adhesive Type (Structural Adhesives, Hot Melt Adhesives, Pressure-Sensitive Adhesives, Polyurethane Adhesives, Acrylic Adhesives, Epoxy Adhesives, and Silicone Adhesives): The structural adhesives segment earned USD 377.8 million in 2023, due to its superior bonding strength, impact resistance, and durability, which enhance vehicle lightweighting, crash safety, and battery enclosure integrity, making it essential for modern EV manufacturing.

- By Substrate (Metals, Plastics, and Composite Materials): The metal segment held 40.12% share of the market in 2023, due to the widespread use of aluminum and steel in EV battery enclosures and structural components, requiring advanced adhesives that ensure strong bonding, corrosion resistance, and durability under high mechanical and thermal stress.

- By Vehicle Type (Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs)): The battery electric vehicles (BEVs) segment is projected to reach USD 3,492.2 million by 2031, owing to the increasing adoption of lightweight adhesive solutions for structural bonding, battery assembly, and thermal management, which are critical for enhancing vehicle efficiency and safety.

- By Application (Battery Assembly, Exterior & Body Structure, Interior Components, and Powertrain & Electronics): The powertrain & electronics segment is poised for significant growth at a CAGR of 24.52% through the forecast period, due to the increasing need for high-performance bonding solutions that enhance thermal management, electrical insulation, and structural integrity in battery packs, inverters, and motor assemblies, ensuring improved efficiency, safety, and durability in EV systems.

Electric Vehicle Adhesive Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

Asia Pacific accounted for a electric vehicle adhesive market share of around 36.87% in 2023, with a valuation of USD 578.2 million. The rapid expansion of domestic EV manufacturing is significantly contributing to the market in Asia Pacific. China leads global EV production, while countries like India, Japan, and South Korea are ramping up efforts to establish large-scale manufacturing hubs.

- The 2024 International Energy Agency (IEA) report states that China recorded 8.1 million new electric car registrations in 2023, reflecting a 35% increase from the previous year. The report also highlights that China exported over 4 million vehicles in 2023, reinforcing its position as the world’s largest auto exporter. Among these exports, 1.2 million were EVs, underscoring the country’s dominance in the global EV market and its expanding influence in international automotive trade.

Increased investments in gigafactories and battery production facilities are driving the demand for adhesives essential in battery pack assembly, thermal interface materials, and vehicle lightweighting.

Adhesive manufacturers are introducing innovative bonding solutions tailored to regional automotive requirements as automakers prioritize efficiency and durability in EV production.

Additionally, the widespread adoption of electric two and three-wheelers is amplifying demand in the market in Asia Pacific. Countries such as India, China, Indonesia, and Vietnam are witnessing a sharp rise in electric scooters, motorcycles, and rickshaws, driven by lower operating costs and government incentives.

These vehicles require specialized adhesives for lightweight structural bonding, electronic component sealing, and battery pack integration. Two wheelers play a crucial role in the region’s electrification strategy, hence adhesive suppliers are developing tailored solutions to meet the specific bonding and durability needs of this growing market.

The electric vehicle adhesive industry in North America is poised for significant growth at a robust CAGR of 23.79% over the forecast period. Surging consumer demand for EVs is accelerating the growth of the electric vehicle adhesive industry in North America. The region has witnessed a sharp rise in EV adoption, driven by improved charging infrastructure, lower operating costs, and increasing model availability.

Companies like Tesla, Ford, and GM are launching high-performance EVs across multiple segments, expanding market penetration. The growing preference for sustainable mobility solutions is pushing automakers to integrate advanced adhesives for battery insulation, thermal management, and impact resistance, ensuring enhanced safety and durability in EVs.

Furthermore, the rapid expansion of EV charging infrastructure is contributing to the growth of the market in North America. Investments in fast-charging networks, battery swapping stations, and grid energy storage are increasing the demand for thermal interface materials, sealants, and high-performance adhesives used in battery packs and power electronics.

Adhesive manufacturers are developing customized solutions to improve the durability and efficiency of charging components as governments and private companies scale up EV charging networks, ensuring seamless integration into the growing EV ecosystem.

Regulatory Frameworks:

- In the U.S., the Toxic Substances Control Act (TSCA), enforced by the Environmental Protection Agency (EPA), mandates chemical registration and risk assessments for adhesives used in EVs. Additionally, the Federal Motor Vehicle Safety Standards (FMVSS), regulated by the National Highway Traffic Safety Administration (NHTSA), set performance and durability criteria for adhesives in vehicle structures and battery packs.

- In Europe, the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) framework, managed by the European Chemicals Agency (ECHA), mandates comprehensive chemical safety assessments for EV adhesives before market entry. Furthermore, the European Committee for Standardization (CEN) and the European Committee for Electrotechnical Standardization (CENELEC) establish technical performance benchmarks for adhesives in vehicle assemblies.

- China’s regulatory framework for EV adhesives is governed by the China Compulsory Certification (CCC), ensuring that products meet national safety and performance standards. Additionally, the Regulations on the Control over Safety of Dangerous Chemicals oversee the production, storage, and use of hazardous substances in adhesives.

- In Japan, the Chemical Substances Control Law (CSCL) mandates pre-market evaluation of chemicals used in EV adhesives, ensuring their safety for human health and the environment. Additionally, Japanese Industrial Standards (JIS) regulate the quality and durability of adhesives in vehicle structures and battery components.

Competitive Landscape:

The global electric vehicle adhesive market is characterized by several market players that are actively expanding their product lines for adhesives in EVs, introducing advanced formulations tailored to evolving industry demands.

Companies are investing in the development of high-performance adhesives with enhanced thermal conductivity, durability, and structural integrity to support next-generation battery technologies and lightweight vehicle designs.

Additionally, manufacturers are scaling up production capacities and establishing new facilities to meet the surging demand for EV adhesives. These strategic initiatives are strengthening market presence, improving supply chain efficiency, and accelerating innovation, thereby contributing significantly to the growth of the market.

- In May 2024, Dow announced the mechanical completion of its new VORATRON Polyurethane Systems adhesive and gap filler production line at its Polyurethanes Systems House in Ahlen, Germany. This expansion will increase the production capacity of VORATRON Polyurethane Systems tenfold, addressing the rising demand for battery assembly materials in the e-mobility sector. These high-strength adhesives and thermally conductive composites play a critical role in meeting the evolving mechanical and thermal management requirements of various EV battery designs.

List of Key Companies in Electric Vehicle Adhesive Market:

- Henkel Corporation

- B. Fuller Company

- Sika AG

- 3M

- PPG Industries, Inc.

- Evonik

- Arkema

- Dow

- Huntsman International LLC

- BASF

- Bostik

- Wacker Chemie AG

- Ashland

- Saint-Gobain

- Parker Hannifin Corp

Recent Developments (Product Launch)

- In February 2025, Panacol-Elosol introduced Structalit 5859, a high-performance adhesive system engineered for magnet bonding in electric motors. Specifically designed for magnet/rotor bonding and securing magnets, this advanced adhesive ensures strong adhesion and long-term durability in demanding operational environments, enhancing the reliability and efficiency of electric motor assemblies.

- In June 2024, WACKER showcased its latest silicone products for battery technology and electromobility at the Battery Show Europe. The event featured the premiere of ELASTOSIL CM 185, specifically designed for application in the sensitive vent and cell contacting system of battery packs. This self-adhesive, condensation-curing formulation delivers an elastomer with enhanced mechanical properties while providing excellent electrical and thermal insulation, making it a valuable solution for advanced battery systems.

- In June 2024, Avery Dennison launched a new range of pressure-sensitive adhesive tape solutions designed for EV battery cell wrapping applications. This latest addition to the company’s EV battery portfolio enhances its lineup of functional tape solutions, specifically developed to mitigate arcing challenges within EV battery packs, ensuring improved safety and performance.

- In January 2024, Arkema achieved a key milestone in decarbonizing its acrylic production chain by obtaining ISCC+ certification for its acrylic acid and ester production facility in Taixing, Jiangsu Province, China. This certification strengthens Arkema’s commitment to sustainability, enabling customers and global partners to develop next-generation eco-friendly materials for specialty coatings and adhesives. These innovations support applications in electronics, EV batteries, renewable energy, and 3D printing, and advancements in home energy efficiency and living comfort.

CHOOSE LICENCE TYPE

CUSTOMIZATION OFFERED

Additional Company Profiles

Additional Company Profiles- Additional Countries

- Cross Segment Analysis

- Regional Market Dynamics

- Country-Level Trend Analysis

- Competitive Landscape Customization

- Extended Forecast Years

- Historical Data Up to 5 Years