Machinery Equipment-Construction

HDPE Pipes Market

HDPE Pipes Market Size, Share, Growth & Industry Analysis, By Product (PE 80, PE 100, Others), By End Use (Agriculture, Water Supply, Oil & Gas, Sewage/Drainage, Chemical, Others), and Regional Analysis, 2024-2031

Pages : 140

Base Year : 2023

Release : February 2025

Report ID: KR1382

Market Definition

The HDPE (High-Density Polyethylene) pipes market involves the production, distribution, and application of HDPE pipes, which are known for their high strength, durability, corrosion resistance, and flexibility.

These pipes are widely used in water supply, sewage systems, agriculture, industrial fluid handling, gas distribution, telecommunications, and mining. Their lightweight nature and ease of installation make them a preferred choice over traditional materials like metal and concrete.

HDPE Pipes Market Overview

The global HDPE pipes market size was valued at USD 21.23 billion in 2023 and is projected to grow from USD 22.15 billion in 2024 to USD 30.62 billion by 2031, exhibiting a CAGR of 4.73% during the forecast period.

This significant growth is attributed to the rising demand for HDPE pipes across various industries, including water supply, sewage management, agriculture, oil & gas, and telecommunications. The increasing emphasis on sustainable and cost-effective piping solutions is propelling the market.

Additionally, HDPE pipes offer superior durability, corrosion resistance, and flexibility compared to traditional materials such as steel and concrete. This increases their appeal in several industries.

Major companies operating in the HDPE pipes industry are DYKA Group, JM EAGLE, INC., Jain Irrigation Systems Ltd., CHINA LESSO, ASTRAL PIPES, supreme.co.in, Advanced Drainage Systems, Chevron Phillips Chemical Company LLC, ISCO Industries, AGRU America, Inc., Alrowad Pipes, Union Pipes Industry, KSA., Harwal Group of Companies, Blue Diamond Industries, and Lane Enterprises, Inc.

Technological advancements in HDPE pipe manufacturing are playing a crucial role in enhancing product quality, efficiency, and performance. Innovations such as improved extrusion processes have led to higher precision in pipe production, ensuring uniform wall thickness, increased strength, and better resistance to external pressures.

These advancements contribute to greater durability and reliability in applications like water supply, sewage management, and gas distribution.

Key Highlights:

- The HDPE pipes industry size was valued at USD 21.23 billion in 2023.

- The market is projected to grow at a CAGR of 4.73% from 2024 to 2031.

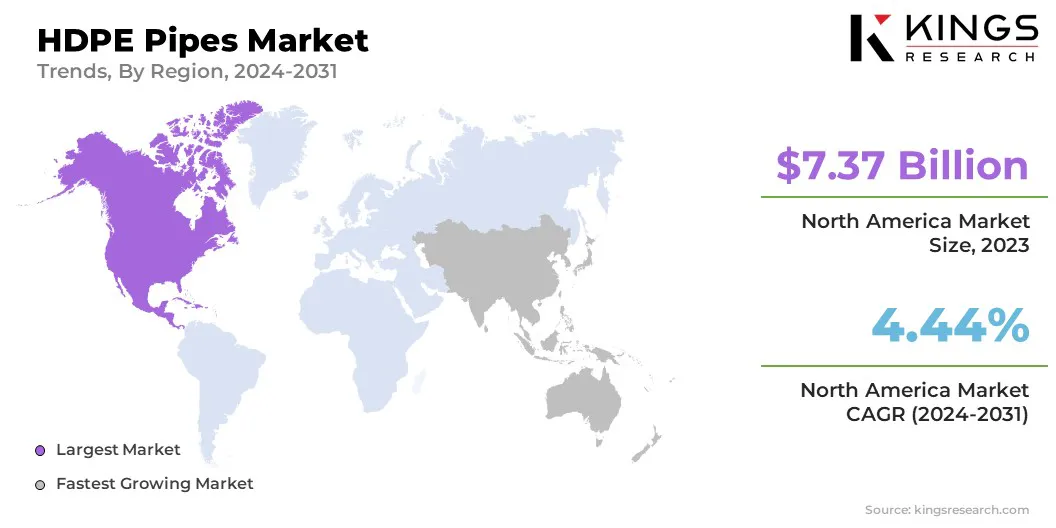

- North America held a market share of 34.69% in 2023, with a valuation of USD 7.37 billion.

- The PE 80 segment garnered USD 9.04 billion in revenue in 2023.

- The water supply segment is expected to reach USD 8.41 billion by 2031.

- The market in Asia Pacific is anticipated to grow at a CAGR of 5.63% during the forecast period.

Market Driver

"Demand for Lightweight Nature, Flexibility, and High-pressure Tolerance"

The HDPE pipes market is driven by the increasing demand for durable, cost-effective, and environmentally friendly piping solutions across multiple industries. One of the primary drivers of the market is the growing need for efficient water management and wastewater treatment infrastructure.

Governments and private sector entities are investing heavily in modernizing water distribution networks, particularly in urban and rural areas where aging pipelines need replacement. HDPE pipes offer superior resistance to corrosion, chemicals, and extreme environmental conditions, making them a preferred choice for water supply, sewage systems, and irrigation.

Another key driver is the rising demand for HDPE pipes in the oil & gas industry. Their lightweight nature, flexibility, and high-pressure tolerance make them ideal for transporting natural gas and other hydrocarbons.

Market Challenge

"Fluctuating Raw Material Prices"

The HDPE pipes market faces a significant challenge in the form of fluctuating raw material prices. HDPE pipes are primarily made from petroleum-based raw materials, and their prices are highly volatile due to fluctuations in crude oil prices. Sudden spikes in raw material costs can disrupt production, increase manufacturing expenses, and squeeze profit margins for manufacturers.

Thus, companies are prioritizing recycling and sustainable polyethylene (PE) sourcing. Using recycled HDPE in production reduces reliance on virgin resin and helps stabilize costs. Additionally, forming strategic partnerships with suppliers enables long-term contracts with fixed pricing, minimizing exposure to market volatility.

Market Trend

"Shift Toward Recycled and Bio-based HDPE Materials"

The HDPE pipes market is increasingly shifting toward recycled and bio-based HDPE materials as sustainability becomes a key industry focus. Amid stringent environmental regulations and corporate sustainability commitments, manufacturers are prioritizing eco-friendly alternatives to reduce dependence on virgin PE.

The use of recycled HDPE helps lower carbon footprints while maintaining the durability and performance required for applications such as water supply, sewage systems, and gas distribution. Governments and industries are actively promoting green infrastructure projects, further driving the demand for sustainable HDPE pipes.

Bio-based PE alternatives are also gaining traction as material science advances, offering long-term growth opportunities in the market.

- For instance, in January 2024, INEOS AG successfully developed the world’s first sustainable gas pipeline using its certified recycled polymer. This milestone demonstrates the growing adoption of recycled HDPE in critical infrastructure, reinforcing the industry's shift toward eco-friendly solutions while ensuring durability and performance in gas distribution networks.

HDPE Pipes Market Report Snapshot

|

Segmentation |

Details |

|

By Product |

PE 80, PE 100, Others |

|

By End Use |

Agriculture, Water Supply, Oil & Gas, Sewage/Drainage, Chemical, Others |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe |

|

|

Asia Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia Pacific |

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

|

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation:

- By Product (PE 80, PE 100, Others): The PE 80 segment earned USD 9.04 billion in 2023, due to its high flexibility, pressure resistance, and cost-effectiveness in various applications, including water supply and gas distribution.

- By End Use (Agriculture, Water Supply, Oil & Gas, Sewage/Drainage, Chemical, and Others): The water supply segment held 28.55% share of the market in 2023, due to increasing investments in modernizing water distribution networks, replacing aging infrastructure, and ensuring efficient water management in urban and rural areas.

HDPE Pipes Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America accounted for around 34.69% HDPE pipes market share in 2023, with a valuation of USD 7.37 billion. This dominance is attributed to high infrastructure investments, particularly in water supply, sewage management, and industrial pipeline networks.

The region's emphasis on sustainable and durable piping solutions has led to increased demand, with government initiatives, funding programs, and regulatory mandates supporting the replacement of aging pipelines.

Additionally, the adoption of HDPE pipes in the oil & gas industry for efficient, corrosion-resistant, and high-pressure transportation further strengthens market growth.

The HDPE pipes industry in Asia Pacific is poised to grow at a CAGR of 5.63% over the forecast period, driven by rapid urbanization, industrial expansion, and increasing infrastructure projects.

Countries like China, India, and Japan are investing heavily in water supply, sewage systems, and agricultural irrigation, boosting the demand for HDPE pipes. Government policies promoting sustainable and cost-effective piping solutions further accelerate market growth.

- For instance, in February 2024, according to the Union Minister of Jal Shakti, India's water infrastructure transformation is driven by a USD 250 billion investment, focusing on modernizing water supply, sewage, and irrigation systems. This decade-long initiative significantly boosts the demand for HDPE pipes, ensuring efficient, durable, and sustainable solutions for urban & rural water management projects across the country.

Regulatory Frameworks

- In the U.S., the ASTM International (American Society for Testing and Materials) regulates HDPE pipes by setting material and performance standards, while the Environmental Protection Agency (EPA) enforces compliance under the Safe Drinking Water Act (SDWA) to ensure safety, quality, and contamination prevention in potable water systems.

- In Europe, the European standards organizations establishes technical standards for HDPE pipes, ensuring consistency in product quality. Relevant standards include EN 12201, which specifies requirements for plastic piping systems used in water supply and sewage.

- In China, the National Standardization Administration of China (SAC) regulates HDPE pipes. It is responsible for establishing and enforcing national standards such as GB/T 13663 for plastic pipes used in water supply.

Competitive Landscape:

The global HDPE pipes market is characterized by a large number of participants, including established corporations and rising organizations. Key players in the market are actively driving innovation and advancing technology to strengthen their market position in a rapidly growing industry.

With applications spanning water supply, sewage management, agriculture, oil & gas, and industrial fluid transportation, companies are continuously enhancing their product offerings to meet sector-specific demands.

Amid significant market expansion, businesses are prioritizing regional penetration and adapting their solutions to local infrastructure needs, regulatory requirements, and environmental sustainability goals, while simultaneously scaling operations to capture opportunities in broader international markets.

- In June 2023, Composite Piping Solutions launched MaxDR, an advanced HDPE pipe technology designed for higher efficiency in trenchless installations. This innovation enhances durability, flexibility, and cost-effectiveness, supporting sustainable infrastructure projects while reducing environmental impact. The launch reflects the industry's shift toward next-generation HDPE solutions for modern pipeline networks.

List of Key Companies in HDPE Pipes Market:

- DYKA Group

- JM EAGLE, INC.

- Jain Irrigation Systems Ltd.

- CHINA LESSO

- ASTRAL PIPES

- supreme.co.in

- Advanced Drainage Systems

- Chevron Phillips Chemical Company LLC

- ISCO Industries

- AGRU America, Inc.

- Alrowad Pipes

- Union Pipes Industry, KSA.

- Harwal Group of Companies

- Blue Diamond Industries

- Lane Enterprises, Inc.

Recent Developments (M&A/Partnerships/New Product Launch)

- In November 2024, Fortress Investment Group acquired Infra Pipe Solutions, a leading HDPE pipes and structures manufacturer, strengthening its position in the infrastructure sector. This strategic move enhances Fortress’s portfolio, leveraging Infra Pipe’s expertise in sustainable piping solutions

- In November 2024, BASF partnered with China’s LESSO Group to develop high-performance HDPE pipes using advanced polymer solutions. This collaboration enhances durability, flexibility, and sustainability in piping systems, supporting China’s infrastructure growth while promoting eco-friendly materials in water supply and construction applications.

CHOOSE LICENCE TYPE

CUSTOMIZATION OFFERED

Additional Company Profiles

Additional Company Profiles- Additional Countries

- Cross Segment Analysis

- Regional Market Dynamics

- Country-Level Trend Analysis

- Competitive Landscape Customization

- Extended Forecast Years

- Historical Data Up to 5 Years

.webp)