BFSI

Pet Insurance Market

Pet Insurance Market Size, Share, Growth & Industry Analysis, By Animal Type (Dogs, Cats, Others), By Coverage Type (Accident Only, Accident and Illness, Wellness Plans, Others), By Sales Channel (Agency, Direct Sales, Bancassurance, Others), and Regional Analysis, 2024-2031

Pages : 190

Base Year : 2023

Release : January 2025

Report ID: KR1240

Market Definition

Pet insurance typically help pet owners manage the cost of routine checkups, vaccinations, surgical procedures, and emergency treatments. Coverage levels may vary, ranging from accident-only policies to comprehensive plans that include wellness care and chronic conditions.

Pet insurance aims to alleviate the financial burden on pet owners, ensuring pets receive timely and adequate medical attention. Policies are often customized based on the species, breed, age, and health condition of the pet, with premiums reflecting these factors.

Pet Insurance Market Overview

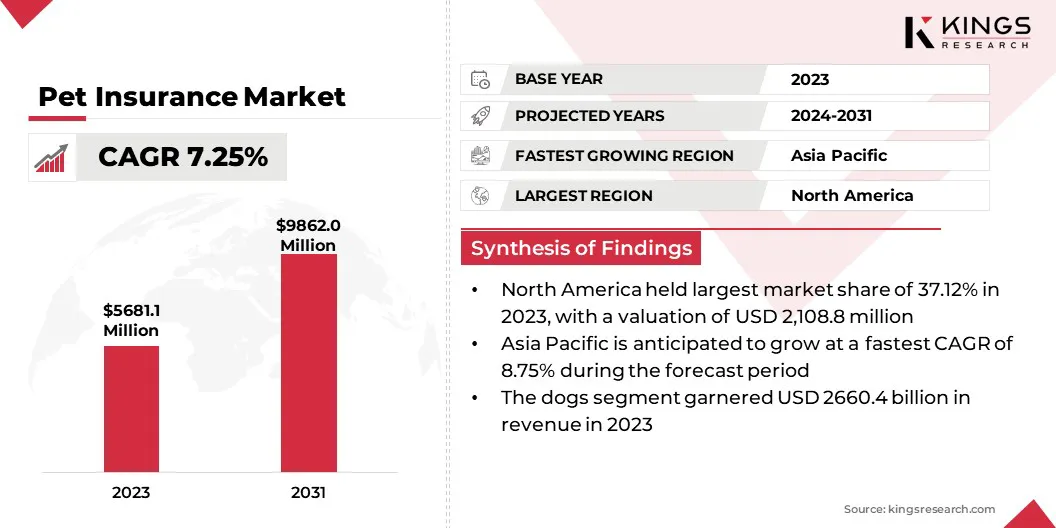

Global pet insurance market size was valued at USD 5,681.1 million in 2023, which is estimated to be valued at USD 6,040.4 million in 2024 and reach USD 9,862.0 million by 2031, growing at a CAGR of 7.25% from 2024 to 2031. The growth of the market is driven by increasing pet ownership globally, coupled with rising awareness of pet health and wellness.

Additionally, the humanization of pets has spurred demand for comprehensive insurance plans. Expanding product offerings and digital solutions are further enhancing accessibility, contributing to the sustained growth of the market.

Major companies operating in the global pet insurance market are Trupanion, Nationwide, Pets Best Insurance Services, LLC, Chubb (Healthy Paws), American Modern Insurance Group, Inc., Allianz Insurance plc (Petplan), Spot Pet Insurance Services, LLC, Figo Pet Insurance LLC, ASPCA, GEICO, MetLife Services and Solutions, LLC, PTZ Insurance Agency, Ltd. (Hartville Group, Inc.), PetFirst, Direct Line, Anicom Holdings Inc., and others.

The global increase in pet ownership has supported the growth of the pet insurance industry. Rapid urbanization and changing lifestyle have prompted individuals and families to adopt pets, with a growing emphasis on treating them as integral members of the household. This trend has led to higher spending on pet healthcare and wellness, creating a robust demand for insurance products.

- The HealthforAnimals report reveals that over half of the global population is believed to own a pet. During the UK's pandemic lockdowns, more than two million individuals adopted pets, while in Australia, pet adoptions surpassed one million at the peak of the pandemic.

Key Highlights:

- The global pet insurance market size was recorded at USD 5,681.1 million in 2023.

- The market is projected to grow at a CAGR of 7.25% from 2024 to 2031.

- North America held a share of 37.12% in 2023, valued at USD 2,108.8 million.

- The dogs segment garnered USD 2,660.4 million in revenue in 2023.

- The accident and illness segment is expected to reach USD 4,203.4 million by 2031.

- The direct sales segment is poised to witness significant CAGR of 8.71% through the forecast period.

- Asia Pacific is anticipated to grow at a CAGR of 8.75% during the forecast period.

Market Driver

"Rising Premium Volume for Pet Insurance"

The increasing total premium volume for pet insurance in several countries highlights the growth potential of the pet insurance market. Rising pet ownership, coupled with greater awareness of comprehensive insurance plans, has led to higher policy adoption rates.

Countries such as the U.S., the UK, and Australia are witnessing significant growth in premium volumes due to robust demand. In the U.S., premium volume has grown steadily due to comprehensive product offerings and a strong emphasis on digital insurance platforms.

- The Insurance Information Institute reported that the total premium volume for pet insurance in the U.S. reached USD 3.9 billion in 2023. By the end of the year, approximately 5.7 million pets were insured in, reflecting a 17% growth compared to 2022. Additionally, total expenditures in the U.S. pet industry rose significantly, increasing from USD 97.1 billion in 2019 to USD 150.6 billion in 2024.

This trend underscores the expanding customer base and willingness of pet owners to invest in their pets' health and wellbeing.

Market Challenge

"Limted Awareness and Understanding of Pet Insurance"

A significant challenge hindering the growth of the pet insurance industry is the limited awareness and understanding of pet insurance among pet owners. Many consumers are unaware of the financial benefits that pet insurance offers, such as mitigating high veterinary bills, particularly for unexpected illnesses or accidents.

To overcome this challenge, companies are adopting various strategies. Insurers are investing in educational campaigns, leveraging digital platforms and social media to highlight the importance of pet insurance. Partnerships with veterinary clinics and pet care providers are being established to promote insurance at the point of care.

Additionally, companies are offering user-friendly tools, such as online policy comparison websites and mobile apps, which allow potential customers to easily assess options and understand coverage.

Furthermore, insurers are introducing flexible plans and trial periods to build trust and encourage first-time policyholders. These efforts aim to foster greater awareness, simplify the decision-making process, and boost market growth.

Market Trend

"Increasing Veterinary Care Costs"

Rising veterinary care expenses have accelerated the demand for pet insurance. Technological advancements in diagnostics, treatments, and surgeries have improved healthcare outcomes for pets, though they also haveled to increased associated costs.

Pet insurance provides financial relief to owners by covering high-cost treatments, making it a vital tool for managing unforeseen medical expenses. This economic benefit, coupled with the growing adoption of advanced veterinary practices, has positioned insurance policies as a practical solution.

- In 2024, the Association of British Insurers (ABI) reported a record-breaking number of pet owners taking out insurance in 2023, reaching 4.4 million policies. A total of 1.8 million claims were filed, marking a 32% increase compared to 2022. Among these, an average of 4,730 daily claims were made for treating sick or injured cats and dogs, representing 1,160 additional daily claims compared to the previous year.

The rising incidence of diseases such as arthritis, cancer, and diabetes in pets has fueled the demand for insurance, contributing to the growth of the pet insurance market. These chronic conditions require ongoing treatment, regular diagnostics, and advanced medical interventions, resulting in substantial healthcare costs.

- The ABI noted that claims for surgery to repair a cruciate rupture in dogs often range from approximately USD 3,800 to USD 6,400. Another common knee condition in cats and dogs, patella luxation, typically costs between USD 2,500 and USD 5,100 to treat. Additionally, the average cost of managing diabetes in cats or dogs is around USD 1,660.

Insurance policies covering long-term treatments provide financial security for pet owners and ensure that pets receive continuous care.

Pet Insurance Market Report Snapshot

| Segmentation | Details |

| By Animal Type | Dogs, Cats, Others |

| By Coverage Type | Accident Only, Accident and Illness, Wellness Plans, Others |

| By Sales Channel | Agency, Direct Sales, Bancassurance, Others |

| By Region | North America: U.S., Canada, Mexico |

| Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe | |

| Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific | |

| Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa | |

| South America: Brazil, Argentina, Rest of South America |

Market Segmentation:

- By Animal Type (Dogs, Cats, and Others): The dogs segment generated a revenue of USD 2,660.4 million in 2023, driven by their status as the most common household pet, coupled with higher veterinary care needs for their size, breed-specific health conditions, and active lifestyles.

- By Coverage Type (Accident Only, Accident and Illness, Wellness Plans, and Others): The accident and illness segment held a share of 41.48% in 2023, mainly due to its comprehensive coverage, addressing the most common and unpredictable health issues affecting pets.

- By Sales Channel (Agency, Direct Sales, Bancassurance, and Others): The agency segment is projected to reach USD 4,207.8 million by 2031, owing to its strong consumer trust and personalized guidance, which enhances customer confidence and increases sales.

Pet Insurance Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

The North America pet insurance market accounted for a share of around 37.12% in 2023, valued at USD 2,108.8 million. Pet owners in North America are increasingly prioritizing their pets' health by seeking preventive care, diagnostic services, and treatments for chronic conditions. This growing awareness of the importance of pet health has led to a rise in demand for health insurance specifically tailored for pets.

- The North American Pet Health Insurance Association (NAPHIA) published its 2024 State of the Industry (SOI) Report, revealing that the North American pet health insurance market experienced a growth of 21.9% in 2023.

Higher income levels, particularly in urban areas, have made it easier for pet owners to prioritize pet insurance, viewing it as an essential investment for their pets' long-term health. Pet insurance has become an important part of financial planning for responsible pet ownership, as owners seek to protect their pets against the rising costs of veterinary care.

- NAPHIA emphasizes that North America is home to an estimated 170.4 million pets, with the pet insurance penetration rate averaging 3.69% in the United States and 3.52% in Canada.

Asia Pacific is set to witness significant growth, registering a robust CAGR of 8.75% over the forecast period. This growth is largely attributed to the increasing use of digital platforms for purchasing pet insurance.

Online channels provide easy access to comparison tools, helping pet owners select insurance plans that best suit their needs, leading to the widespread adoption of pet insurance products in the region.

- In December 2024, Zhibao Technology Inc. in China entered the pet insurance sector through its subsidiary, Sunshine Insurance Brokers, launching "Chong Bao Bao," an online platform and brand dedicated to providing pet insurance solutions in China. Pet medical and liability insurance now join Zhibao's expanding portfolio of over 40 digital insurance solutions that span various industries and products.

- In December 2024, MSIG Singapore formed a partnership with pet supplies distributor Silversky and insurance startup Stere Asia to introduce digital pet insurance. The product, named Silversky Protect, is underwritten by MSIG and integrates smoothly into Silversky's digital platform through Stere Asia's API technology.

Regulatory Framework Also Plays a Significant Role in Shaping the Market

- In the U.S., the National Association of Insurance Commissioners (NAIC) adopted the Pet Insurance Model Act in August 2023. This act establishes standardized guidelines for policy disclosures, claims handling, and consumer protections within the pet insurance industry. The model act aims to ensure transparency and fairness, providing a framework for states to regulate pet insurance effectively.

- The European Insurance and Occupational Pensions Authority (EIOPA) provides oversight and guidelines for insurance products, including pet insurance, within EU member states. EIOPA's regulatory framework focuses on consumer protection, transparency, and the stability of the insurance market. Specific regulations may vary by country. However, EIOPA sets the overarching standards that national regulators implement.

- In the United Kingdom, pet insurance providers are regulated by the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA). These regulatory bodies oversee the financial stability of insurers and ensure fair treatment of consumers.

- In October 2023, the Financial Services Commission (FSC) in South Korea proposed measures to enhance pet insurance services. These initiatives aim to improve product offerings and consumer satisfaction within the pet insurance market, while emphasizing the need for a supportive regulatory environment.

Competitive Landscape:

The global pet insurance market is characterized by a large number of participants, including both established corporations and rising organizations. Leading companies are increasingly adopting strategic partnerships to drive market expansion and enhance their offerings.

By collaborating with key industry players, such as pet care providers, veterinary clinics, and digital platforms, these companies are able to integrate innovative solutions that meet the evolving needs of pet owners.

These strategic partnerships are critical in fostering market growth, allowing companies to offer more comprehensive, accessible, and tailored insurance products that meet the demands of a diverse and growing market.

- In January 2024, Nationwide, aleading pet insurer, partnered with Petco Health and Wellness Company, Inc. to deliver affordable, integrated pet health, wellness, and protection solutions through a new customizable pet health insurance plan. This offering provides essential coverage for unforeseen veterinary costs due to accidental injuries, including broken bones, lacerations, poisoning, and other incidents.

List of Key Companies in Pet Insurance Market:

- Trupanion

- Nationwide

- Pets Best Insurance Services, LLC

- Chubb (Healthy Paws)

- American Modern Insurance Group, Inc.

- Allianz Insurance plc (Petplan)

- Spot Pet Insurance Services, LLC

- Figo Pet Insurance LLC

- ASPCA

- GEICO

- MetLife Services and Solutions, LLC,

- PTZ Insurance Agency, Ltd. (Hartville Group, Inc.)

- PetFirst

- Direct Line

- Anicom Holdings Inc.

Recent Developments

- In June 2024, Trupanion, Inc., a leading pet insurance provider, partnered with Boehringer Ingelheim, a global leader in animal disease prevention and treatment innovation, to offer pets and their families improved access to high-quality healthcare, along with enhanced disease treatment and protection.

- In April 2024, MetLife Pet Insurance collaborated with the Association of Animal Welfare Advancement (AAWA) to support pet parents in confidently caring for their pets throughout their lives. This collaboration aims to develop and produce content that addresses the challenges pet parents face, particularly related to access to veterinary care.

- In April 2024, Chubb finalized an agreement to acquire Healthy Paws, a U.S.-based managing general agent (MGA) specializing in pet insurance. As part of Chubb, Healthy Paws will enable more pet owners to manage the rising costs of veterinary care and secure funding for their pets' medical needs.

- In August 2024, Petplan launched a new mobile app that includes telemedicine services, enabling pet owners to consult veterinarians remotely. This innovation enhances the convenience of Petplan's offerings, appealing to tech-savvy customers and those seeking more accessible veterinary care.

CHOOSE LICENCE TYPE

CUSTOMIZATION OFFERED

Additional Company Profiles

Additional Company Profiles- Additional Countries

- Cross Segment Analysis

- Regional Market Dynamics

- Country-Level Trend Analysis

- Competitive Landscape Customization

- Extended Forecast Years

- Historical Data Up to 5 Years